It isn’t necessary to have intimate knowledge of the backend working of the back card system in order to find the best card processing system. But it’s a good idea to have a general understanding of how card processing works and the types of fees charged at various stages of the system.

This blog is on the key functionality of card processing services that will help you reach a better understanding of card processing. You’ll have in-depth details about what defines a payment solution provider, how processing works, the fees involved while doing any transaction, and the risk.

Actors Involved in Card Processing

The card processing company handles the processing and batching of purchases made with credit, debit, or gift card payments. They typically assist with technology needs and customer service, wherein they act as an intermediary between card associations and banks.

There are multiple stakeholders involved when a customer swipes their card at POS. The information below helps to summarize the essential roles involved in payment processing.

Cardholder

If you have a credit or debit card (as most of us do), you’re already familiar with the role of the cardholder. But just to give you knowledge-a cardholder is someone who obtains a card (debit or credit) from a card issuing bank which they eventually use to purchase goods or services both online or office at the store.

Merchant

Technically, a merchant is any business that sells goods or services. But, only merchants that accept cards as a form of payment are pertinent to our explanation. So with that said, a merchant is any business that maintains a merchant account that enables them to accept credit or debit cards as payment from customers (cardholders) for goods or services provided.

Acquiring Bank (Merchant’s Bank)

An acquiring bank is often referred to as a merchant bank as they contract with merchants to create and maintain accounts that allow the business to accept credit or debit card payments. Acquiring banks provide merchants with equipment and software to accept cards and handle customer service and other necessary aspects involved in card acceptance. An acquiring bank is a registered member of the card association (Visa, RuPay, and MasterCard)

Issuing Bank

You have probably guessed the role of issuing banks by their name itself. The issuing bank is also a member of the card association(Visa, MasterCard, or RuPay)

Card Association

Visa, MasterCard, or RuPay aren’t banks and they don’t issue cards or merchant accounts. Instead, they act as a custodian and clearinghouse for their respective card brand. They also function as the governing body of financial institutions, ISOs, and MSPs that work together in association to support card processing.

Primarily, card associations govern the members of their association, including interchange fees and qualification guidelines, act as the arbiter between the issuing and acquiring banks among other vital functions.

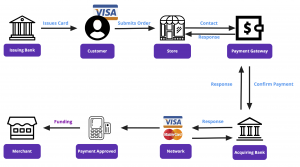

What does card processing look like in motion?

Card processing basically works in conjunction with three distinct processes:

- Authorization

- Settlement

- Funding

First, let’s take a look at the authorization process.

- The cardholder swipes the card at the merchant POS in exchange for goods or services.

- The merchant sends a request for payment authorization to their payment processor.

- The payment processor submits transactions to the appropriate card association, eventually reaching the issuing bank.

- Authorization requests are made to the issuing bank, including parameters such as CVV, expiration date, etc validation.

- The issuing bank approves or declines the request. The transaction can be declined in case of insufficient funds.

- The issuing bank then sends the approval (or denial) statement back along the line to the card association, merchant bank, and finally to the merchant.

That’s the card authorization process in a nutshell.

Now let’s take a look at the settlement and funding

- Merchants send batches of authorized transactions to their payment processor.

- The payment processor passes transaction details to the card associations that communicate the appropriate debits with the issuing bank in their network.

- The issuing bank charges the cardholder’s account for the amount of the transactions,

- The issuing bank then transfers the appropriate amount for the transactions to the merchant bank, minus the interchange fees.

- The merchant bank deposits funds into the merchant account.

That’s the simplified card payment processing system wherein the authorization takes a matter of seconds. Settlement and funding that used to take days are now always handled overnight, helping you get your money quickly.